INNOVATION KEEPS THE AD MARKET MOVING

KEY FINDINGS

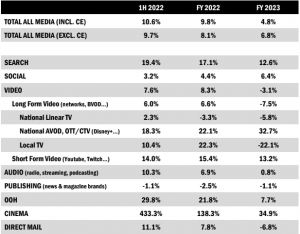

• In the wake of a historically strong 2021, U.S. media owner’s advertising revenues grew by +11% to $151 billion in the first half of 2022, based on financial reports.

• Media channel performance varied greatly in the first half with strong revenue growth in out-of-home (+30%), and robust growth in keyword formats (search, retail media) (+19%), contrasted against stagnation in social media (+3%).

• The weaker economic environment will cause several industry verticals to reduce ad spend in the second half, but stronger-than-expected political spending will mitigate the impact on revenues of media owners.

• Full-year media owner revenues will thus cross the $300bn market for the first time, to reach $323bn. That’s +9.8% above 2021 levels (+8.1% if we only consider non-cyclical ad spend and exclude political dollars).

• For 2023, the continued economic slowdown and the lack of major cyclical events led MAGNA to reduce its growth forecast to +4.8% from +5.8% in the previous report.

• MAGNA expects Entertainment (Movies, Streaming), Travel and Betting to grow advertising spending next year, possibly joined by Automotive as the car market finally stabilizes.

• Keyword search formats (+13%) and OOH (+8%) will continue to outperform, while long-form AVOD spending will be driven by the addition of ad-supported tiers from Disney+ and Netflix (+33%).

Vincent Létang, EVP Global Market Intelligence at MAGNA and author of the report, commented: “Following a strong first half, non-cyclical advertising spending is slowing down as several industries are facing an uncertain economic environment. There are several growth factors that will help stabilize media owner ad revenues in coming months, however. In the short-term (2H22) cyclical factors: Billions of ad dollars will be spent by political campaigns in TV, direct mail, and digital media. In the mid-term (2023) there will be multiple organic growth factors, driven by marketing technology innovation: Retail media networks bringing below-the-line marketing budgets into digital media, programmatic spending in digital audio and digital OOH formats, and the expansion of AVOD and CTV advertising with new ad-supported tiers from Disney+ and Netflix.”

FIRST HALF RECAP: A STRONG START FOR AD SPEND

Based on the analysis of media owner’s financial reports, MAGNA estimates that total net advertising sales grew by +11% year-over-year in the first half of 2022 to reach $151 billion. Ad sales grew by +14% year-over-year in the first quarter, and by +7% in the second quarter (+4% above first quarter).

OOH was the fastest growing ad format (+30% year-over-year). OOH media is driven by the recovery of consumer mobility since January and return of national and local advertisers following the deep COVID decline in 2020. MAGNA just published a detailed report on global OOH trends, looking at the growth of OOH ad sales in the U.S. and internationally. Cinema advertising grew by +430% in the first half, as both blockbusters and moviegoers finally returned en masse into theaters.

Other growth formats in 1H22 included Search (+19%), Digital Audio (audio streaming and podcasting, +19%), AVOD/CTV (Hulu, Peacock, etc. +18%) and short-form digital video formats (YouTube, Twitch, etc. +14%).

On the other hand, social media ad sales continued to slow down dramatically, from +38% in 2021 to +7.5% in the first quarter and -1% in the second quarter, to end the first half up by just +3% to $30 billion. Social media apps continue to suffer from the reduced access to user data in the iOS environment, which impacts the attractiveness and pricing power of social ad formats, while total social media usage has reached maturity.

Meanwhile, traditional linear ad sales slowed down in the first half. National television sales increased +2% to $20bn, partly thanks to incremental ad sales around Beijing Winter Olympics. Local TV sales rose +10% to $9bn in the first half, thanks to political spending, or +2% on an underlying basis.

SECOND HALF AND FULL YEAR 2022: CYCLICAL DOLLARS HELP MITIGATE THE IMPACT OF ECONOMIC SLOWDOWN

Economic uncertainty and rising inflation are affecting several industries and driving brands and local businesses to moderate their marketing expenses in the second half. CPG verticals (food, drinks, personal care, and household goods) are especially at risk as they are forced to increase product prices and face the possibility of consumers trading down in favor of cheaper brands. Restaurants and retail face a similar business challenge while some industries, like mortgage lenders, see their businesses suffer from the rise of interest rates.

As a result, MAGNA anticipates non-cyclical ad spend will slow down to +6.6% in the second half. This will be offset by the record influx of cyclical ad spend around the mid-term elections and the soccer World Cup in November. Based on unprecedently large fund-raising year-to-date, MAGNA expects political advertising spending to grow by +63% over the previous mid-term cycle (2018) and generate $7.3 billion in incremental advertising revenue for media owners, with 70% of it concentrated in the second half. Local television will attract almost two-thirds of that total, as political ad sales will account for 25% of total local TV ad revenue this year (and more for stations in “battleground” markets). Digital media formats will receive $1.3 billion from political campaigns, with sales up between +150% and +200% for search, digital video, and social formats.

With a strong first half and political advertising mitigating the slowdown in the second half, MAGNA expects full-year, all-media advertising revenues to surpass the $300bn mark for the first time and reach $323bn this year. That represents an increase of $29 billion over 2021 (+9.8%), with non-cyclical underlying growth at +8.1%.

On a full-year basis, cross-platform video will grow by +8% (linear television -3%, local TV +22%, AVOD +22%). Cross-platform audio (radio, audio streaming) will increase by +7%, OOH by +22% and cinema by +138%. Among “direct” media formats, search will grow by +17%, direct mail by +8% and social media by +4%.

2023: ORGANIC FACTORS KEEP THE AD MARKET GROWING

The lack of major cyclical events and the weakness of the economic outlook has led MAGNA to reduce its advertising forecast for 2023.

In terms of industry spending, MAGNA anticipates below-average growth for CPG verticals, Finance and Retail. On the other hand, Entertainment ad spend will grow from the continued recovery of moviegoing and re-ignited competition in the AVOD/SVOD industry. Travel will continue to recover, and Online Betting will develop further as more large states (Ohio for sure, possibly Texas, California and Florida) may legalize the activity at some point during the year. Finally, there’s hope that the Automotive vertical may start to recover in 2023 after two years of decline in car sales and advertising activity. Car sales have stabilized since August, mostly due to a comparison effect (they had started to fall a year before), and, as soon as the supply-chain conditions and production capacities improve, manufacturers and car dealers will compete again to meet the pent-up demand.

Nevertheless, MAGNA still expects total ad revenue to grow in 2023 (+4.8% vs. +5.8% in our prior forecast) thanks to organic drivers, many of them derived from innovation in media offering and media technology. Among these:

The rise of retail media networks. Retail media advertising will increase from $31 billion this year to $42 billion in 2023. The bulk of it comes from Amazon’s product search but all other large retailers are now developing advertising sales through keyword search or display ads on their apps and websites. Retail media is mostly fueled by consumer brands reallocating below-the-line, trade-marketing budgets from in-store towards digital retail networks, as a greater percentage of retail sales comes from e-commerce. Furthermore, retail-owned media networks are mostly immune from the privacy-based limitations on data usage and targeting, that display or social media owner’s face, because they can leverage their own first-party data.

The expansion of AVOD. The transition from linear to on-demand, CTV-based television has been going on for 10 years, and it has been mostly SVOD-centric until now. The imminent launch of cheaper, ad-supported tiers from both Netflix and Disney+ will expand the reach and ad inventory offered by AVOD. While the two new offerings may take ad budgets from other media properties (AVOD or linear TV) MAGNA believes these new offerings will “grow the pie” rather than cannibalize existing budgets or incumbent vendors like Hulu, Peacock, Paramount+ and “FAST” channels, which will continue to grow. As a result, the long-form AVOD/CTV segment will accelerate from +22% in 2022 to +33% in 2023, to reach $6.3 billion in total advertising sales.

Next MAGNA forecast (U.S. and Global): December 2022

U.S. NET ADVERTISING REVENUE: GROWTH FORECASTS

ABOUT THE RESEARCH

The MAGNA research is media centric. It monitors net media owners advertising revenues based on a bottom-up analysis of financial reports and data from media trade organizations; other ad market studies are based on tracking ad insertions or consolidating agency billings. The MAGNA approach provides the most accurate and comprehensive picture of the market as it captures total net media owners’ ad revenues coming from national consumer brands’ spending as well as small, local, “direct” advertisers. Forecasts are based on economic outlook and market shares dynamic. The full report contains more granular media breakdowns and forecasts to 2025, for 70 markets.

Next Global Forecast: December 2022 – Next U.S. Forecast: September 2022.

ABOUT MAGNA

MAGNA is the leading global media investment and intelligence company. Our trusted insights, proprietary trials offerings, industry-leading negotiation and unparalleled consultative solutions deliver an actionable marketplace advantage for our clients and subscribers.

We are a team of experts driven by results, integrity and inquisitiveness. We operate across five key competencies, supporting clients and cross-functional teams through partnership, education, accountability, connectivity and enablement. For more information, please visit our website: https://www-wp-stage.magnaglobal.com/and follow us on LinkedIn and Twitter.

MAGNA has set the industry standard for more than 60 years by predicting the future of media value. We publish more than 40 reports per year on audience trends, media spend and market demand as well as ad effectiveness.

To access full reports and databases or to learn more about our market research services, contact [email protected].