After two quarters of stagnation, US advertising spending re-accelerated to +4.4% year-over-year in the second quarter, but digital media formats were the only ones to see a significant improvement in advertising sales. The digital advertising recovery, combined with a slightly better economic outlook, led MAGNA to raise its market growth forecast for 2023 and 2024.

KEY FINDINGS

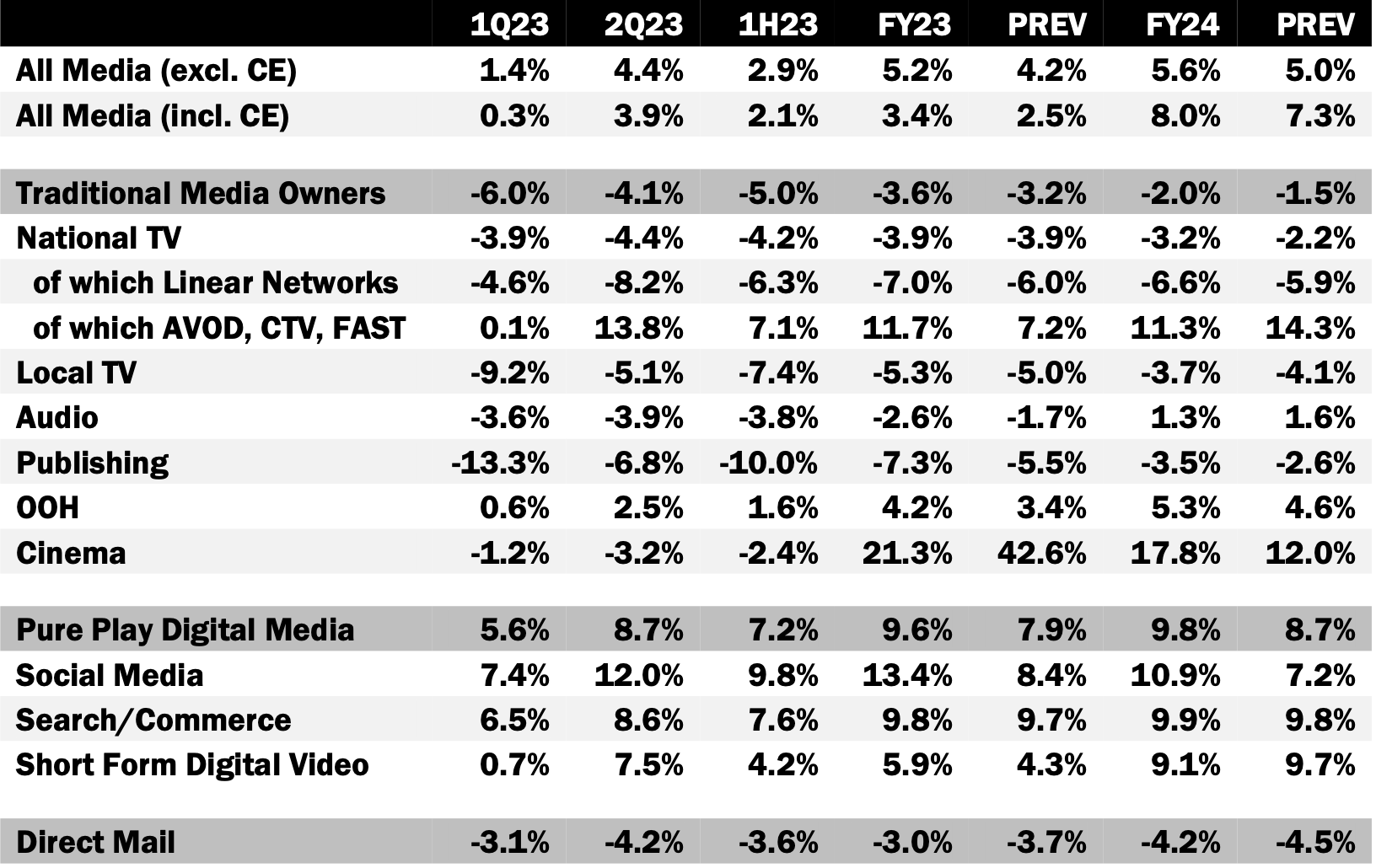

- Total advertising spending re-accelerated in the second quarter of 2023. Sales were up +4.4% year-over-year, following two quarters of stagnation.

- However, only pure-play digital media vendors (Search, Social, Video) really benefited (+8.7% in 2Q23), while traditional media companies continued to struggle (-4.1% in 2Q23).

- The recovery in ad spend in 2Q23 was caused by a general improvement in the economy, and easier yoy comps.

- The better economic outlook and continued influx of retail media dollars into digital ad formats lead MAGNA to raise its full-year, all-media ad spend 2023 forecast by one percentage point, to +5.2% (digital media owners +9.6%, traditional media owners -3.6%).

- Looking at 2024, MAGNA raises the ad spend forecast from +5.0% to +5.6% (+8.0% including cyclical spend).

- Digital media owners will grow ad sales by +9.8% next year, while cyclical spending will mitigate the erosion of non-cyclical ad sales for traditional media owners (-2.0% excl. cyclical, +4.3% including cyclical/political).Vincent Létang, EVP Global Market Intelligence and author of the report, said: “Six months ago, the media industry was bracing for recession, but advertisers kept calm and continued to support their brands and sales through media investment. As the US economy and advertising spending were both stronger than expected so far this year, and digital media is finally recovering from its 2022 woes, MAGNA raises its full-year ad revenue growth forecast to +5.2% for 2023 to reach $337 billion.”FIRST HALF 2023: DIGITAL SPENDING RECOVERS BUT TRADITIONAL MEDIA CONTINUE TO STRUGGLEBased on MAGNA’s analysis of media companies’ financial reports, ad revenue and ad spend recovered in the second quarter. Advertising sales grew by +4.4% year-over-year, close to but slightly stronger than MAGNA’s June expectation of +3.6%, following two quarters of stagnation (+1% yoy in 4Q22 and 1Q23). Overall, the US ad market was up by +2.9% in the first half (excluding cyclical), against hard comps.

However, only pure-play digital media formats (Search, Commerce, Social, Pureplay Short-Form Video) really benefitted from the increased ad spend so far (+8.7% yoy in 2Q23, up from +5.6% in 1Q and +7.2% for 1H23). Meanwhile traditional media companies (TV, radio, publishing, out-of-home, cinema) struggled with eroding ad sales (-4.1% in 2Q23 after -6.0% in 1Q23).

Ad sales grew by almost +12% for Social media formats in the second quarter, compared with +7% in 1Q23 and almost zero in the two previous quarters. Short-form digital video (Youtube, Twitch or outstream video) re-accelerated to +7.5% from zero in 1Q and Search/Commerce remained robust at almost +9%, driven by retail media activity. When it comes to traditional media owners, 2Q23 was marginally better than 1Q23 but most ad formats continue to suffer declining sales. Cross-platform national TV ad sales and Audio ad sales were down -4%, local TV -5%, Publishing -7%. The only traditional media category to grow in first half was OOH with +2.5% in the second quarter.

The ad revenues of traditional media owners continue to stagnate or decline despite the growth of their digital formats. In the first half of 2023, non-linear TV ad sales (AVOD, CTV, FAST…) grew by +7%, podcasting advertising grew by +14% and DOOH grew by +9%. But so far, the attractiveness of these new formats for consumers and advertising is just mitigating, not offsetting, the long-term decline of traditional linear formats in audience and ad sales.

ECONOMIC OUTLOOK AND SPENDING VERTICAL: A MIXED BAG

The recovery in advertising spending in 2Q23 was caused by easier comps and by a general improvement in the economy, as well as easier yoy comps. Real GDP grew by +2.4% (annualized) in the second quarter, much better than the +1% expected in May. Inflation continued to recede (core consumer inflation index down to +3.3% in August) while consumer confidence gradually improved (index 70 in August vs index 50 a year ago); unemployment remains under 4%.

One source of concern is retail sales, which slowed down to -0.6% yoy in June, and may lead some consumer brands to restrict marketing budgets and advertising spending.

Around the average advertising spending growth of +4.4% in 2Q23, MAGNA observed a strong dynamic from Travel, Pharma and Retail brands, and – more surprisingly – CPG (food, drinks, personal care). The slowdown of inflation in recent months may explain this recovery in CPG brand business and marketing spending, after a difficult year 2022 when high inflation hurt the sales of premium brands. Ad spend was flat or slightly up for Auto and Entertainment brands. This is disappointing in the case of Automotive, as the strong recovery of the car market (+15%) hasn’t fully translated into marketing activity acceleration so far – at least not for traditional media. It may be because Auto advertising didn’t dip that much when car sales declined in early 2022 and manufacturers pivoted towards long-term marketing goals, e.g. pushing EVs rather than supporting short-term sales. Finally, as expected, Finance and Technology, two rather large verticals, are down year-over-year.

Let’s keep in mind that these trends are for total ad spend, including digital media formats. If we look at traditional media spending only, most key verticals are spending less than last year except Travel and Pharma, which are relatively small spending verticals.

2023 FULL-YEAR AD FORECAST RAISED TO +5.2%

With the economic outlook improving and yoy comps becoming even easier, MAGNA maintains its growth forecast for the second half of the year. Total ad spend will grow by +7% to +8% in 3Q23 and 4Q23 (compared to +2.9% in first half) to bring full year growth to +5.2% (excluding cyclical), up from +4.2% in our previous update (June 2023).

MAGNA raises the 2023 revenue forecast for digital media owners (the Google, Meta, and Amazons), from +7.9% to +9.6% but downgrades the ad revenue expectation for traditional media owners in radio, television, publishing, and OOH, from -3.2% to -3.6%. Digital pure players will capture a record 69% of total ad spend in 2023 with the big thee alone capturing 59%.

2024: DIGITAL FORMATS ACCELERATE, CYCLICAL AD SPEND STABILIZES TRADITIONAL MEDIA

Looking at 2024, the easy first half comps and influx of retail media dollars into digital advertising lead us to increase the non-cyclical growth forecast from +5.0% to +5.6%. We raise the growth forecast for pure-play digital media owners to +9.8% but the forecast for traditional media owners is downgraded to -2.0% from -1.5%. Incorporating cyclical events (political ad spend, and additional spending around summer Olympics) the revenue forecast for traditional media owners will reach +4.3% and the grand total will reach +8.0% to $364bn.

Looking at individual media types, digital media formats will outperform again in the next 18 months, growing by high-single digits or low double-digits. Social media formats and short-form digital video formats are finally recovering from the headwinds and disruptions that hurt ad sales in 2022, brought on by the modifications to privacy settings in the Apple environment and the rapid rise of short vertical video snacking. Social and short video formats are expected to grow ad revenues by +10.9% and +9.1%, respectively. These formats are mature, however, and MAGNA does not expect annual growth rates to ever grow back to the +20% or +30% that were observed pre-COVID or in 2021.

Search/Commerce formats will continue to be boosted by retail media activity. Retail media networks are already generating 30% of search advertising sales (including Amazon) and this will grow by +22% in 2023 and +17% in 2024. Total search, including traditional search engines like Google, will grow by +9.8% in 2024 to $143bn.

The ad revenues of most traditional media owners will continue to stagnate or decline despite the continued growth of their digital ad sales. Non-cyclical ad sales will be down -3% for national TV and -5% for local TV next year. However, spending around the summer Olympics upcoming Presidential election will mitigate the revenue erosion for national TV and bring huge growth for local TV. Local TV ad revenues are expected to grow by +28% compared to 2023, thanks to an incremental $5.7 billion generated by political demand and induced spot inflation.

Meanwhile national TV networks are facing challenges on two fronts in 2024, on both volumes and pricing supply. The ongoing writers’ strike may lead to a lack of fresh attractive content in the first half of 2024 and thus potentially a further acceleration in long-term viewing declines. In addition, the loss in ratings will not be offset by pricing since MAGNA predicts low-single digit CPM inflation for the first time in 20 years. As a result, non-cyclical linear ad sales will shrink by almost -7% next year, but that will be mitigated by the continued rise of AVOD ad sales (+11%) and $800 million of incremental revenues generated around the Paris Olympics. Total cross-platform national TV ad revenues will thus shrink by just -0.7% next year (compared to -3% excl. CE), to $46.4bn.

Other media types typically attract very little cyclical ad dollars, but the scale and growth of digital audio formats (streaming, podcasting) will offset the decline in broadcast radio to stabilize total audio revenues (+1.3% to $16.5bn), while OOH advertising will grow by +5% next year to $9.9bn. Direct mail sales will drop -4% in 2024 excl. CE, but will generate $800m in political spending that will mostly mitigate the underlying structural decline (sales incl. CE: -1%).

A 11-minutes video presentation of this research is available here.

The next MAGNA Ad Forecast (US and Global) will be published early December.

MAGNA AD FORECAST – FALL 2023 UPDATE – KEY FIGURES

Source: MAGNA US Ad Forecast, September 2023. Mediabrands clients and MAGNA subscribers can access full report and dataset including additional media granularity and long-term forecasts.

Source: MAGNA US Ad Forecast, September 2023. Mediabrands clients and MAGNA subscribers can access full report and dataset including additional media granularity and long-term forecasts.

ABOUT MAGNA MARKET INTELLIGENCE

MAGNA market intelligence is media centric. It estimates net media owners advertising revenues based on an analysis of financial reports and data from local trade organizations; other ad market studies are based on tracking ad insertions or consolidating agency billings. The MAGNA approach provides the most accurate and comprehensive picture of the market as it captures total net media owners’ ad revenues coming from national consumer brands’ spending as well as small, local, “direct” advertisers. Forecasts are based on economic outlook and market shares dynamic.

ABOUT MAGNA

MAGNA is the leading global media investment and intelligence company. Our trusted insights, proprietary trials offerings, industry-leading negotiation and unparalleled consultative solutions deliver an actionable marketplace advantage for our clients and subscribers.

We are a team of experts driven by results, integrity, and inquisitiveness. We operate across five key competencies, supporting clients and cross-functional teams through partnership, education, accountability, connectivity, and enablement. For more information, please visit our website: https://www-wp-stage.magnaglobal.com/ and follow us on LinkedIn.

MAGNA has set the industry standard for more than 60 years by predicting the future of media value. We publish more than 40 reports per year on audience trends, media spend and market demand as well as ad effectiveness.

To access full reports and databases or to learn more about our market research services, contact [email protected].